How to Decide the Best Age to Claim Social Security in Retirement

One of the most important financial decisions retirees make is when to begin Social Security benefits.

You can claim as early as age 62, wait until full retirement age (FRA), or delay until age 70. Each choice has long-term income and tax implications.

The right decision depends on:

-

Life expectancy

-

Other retirement income sources

-

Tax planning strategy

-

Spousal benefits

-

Overall retirement goals

Understanding how benefits grow over time is critical. Deciding when to take Social Security should be coordinated with your broader retirement withdrawal strategies.

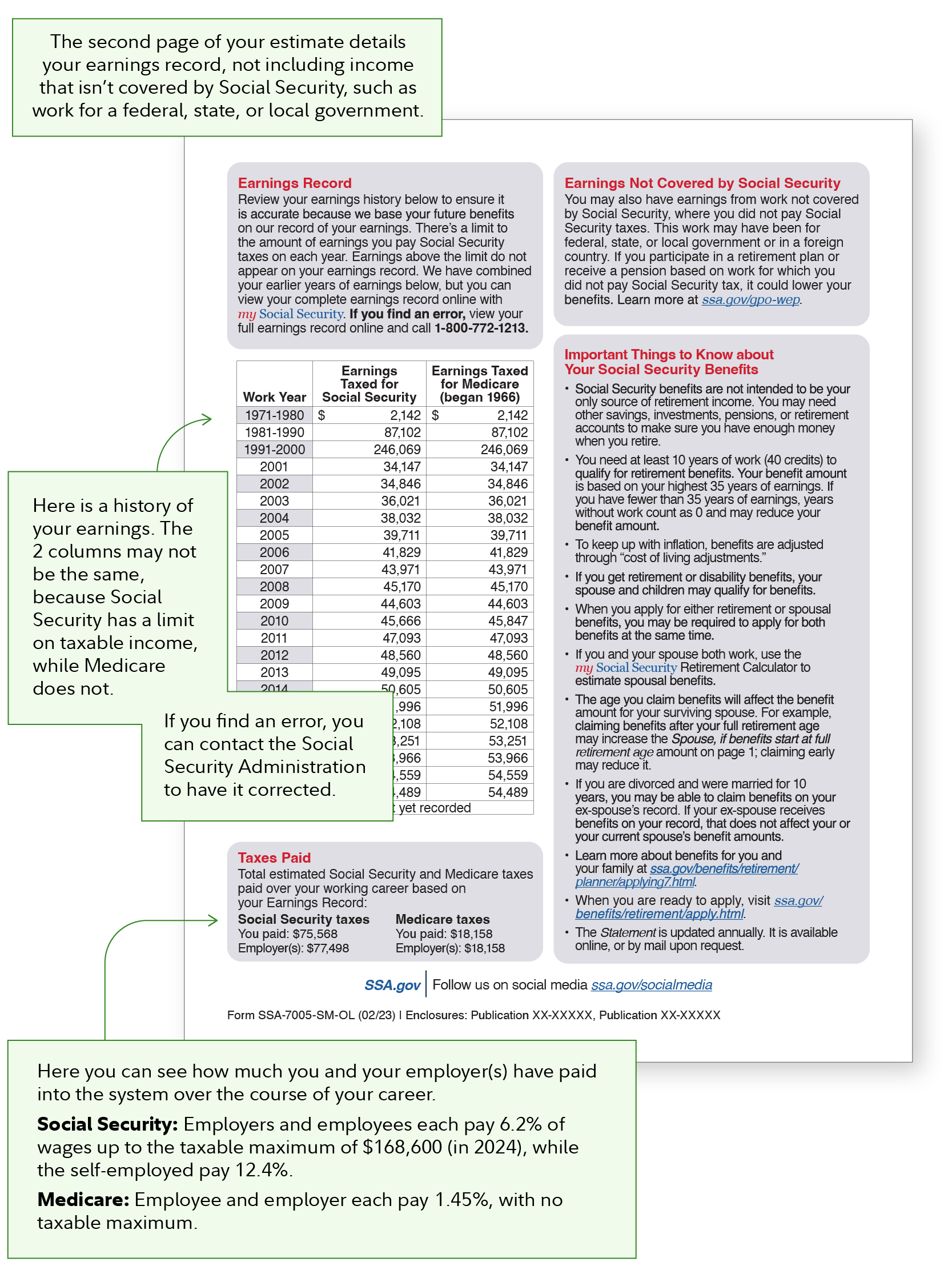

How Social Security Benefits Increase

According to the Social Security Administration:

-

Claiming at 62 results in a permanent reduction (up to 30% lower than full retirement age).

-

Claiming at full retirement age (66–67, depending on birth year) provides 100% of your benefit.

-

Delaying benefits increases payments approximately 8% per year until age 70.

(Source: SSA Benefits Planner, 2024)

That increase is called Delayed Retirement Credits.

Full Retirement Age (FRA) Matters

Your full retirement age depends on your birth year. For individuals born in 1960 or later, FRA is age 67. Claiming before FRA permanently reduces monthly benefits.

Claiming after FRA increases them. This can also affect your spouse’s benefits and election amount.

(Source: SSA Retirement Benefits, 2024)

Longevity and Break-Even Analysis

A common question is:

“Should I take benefits early or wait?”

The old saying, “bird in hand vs. two in the bush.” If you live into your late 70s or 80s, delaying benefits often results in higher total lifetime income. If longevity is shorter, early claiming may result in more total dollars received. There is no right answer. One way to look at this is that it comes down to your own health, longevity in your family tree, life goals, and the amount of money saved to produce income to reach those goals.

According to data from the Social Security Administration, the average life expectancy for someone reaching age 65 is well into the 80s. Coordinating benefits with income planning can help avoid common tax planning mistakes retirees should avoid.

(Source: SSA Actuarial Life Table, 2024)

Taxes and Social Security

Social Security benefits may be taxable depending on your total income. Up to 85% of benefits can be subject to federal income tax if provisional income exceeds certain thresholds. Keep in mind if you are retiring early and want to get insurance through the open healthcare market. Social Security counts as income and goes towards if you qualify for a subsidy.

(Source: SSA Income Taxes on Benefits, 2024)

This is why timing Social Security often ties directly into broader retirement tax planning.

Spousal and Survivor Benefits

Married couples have additional planning opportunities:

-

Coordinating claiming strategies

-

Considering survivor income needs

-

Evaluating age differences between spouses

For married retirees, delaying the higher earner’s benefit can increase survivor income if one spouse passes away first.

(Source: SSA Spousal Benefits Guidance, 2024)

Health, Cash Flow & Other Considerations

Beyond math, factors include:

-

Health history

-

Need for immediate income

-

Employment status

-

Market conditions

-

Portfolio withdrawal strategy

Social Security is often the only inflation-adjusted lifetime income source retirees have.

That makes the decision strategic, not just mathematical. Claiming too early is often cited among the most common Retirement Regrets and How to Avoid Them.

Sources

Social Security Administration. (2024). Retirement benefits planner. https://www.ssa.gov

Social Security Administration. (2024). Income taxes and your Social Security benefits. https://www.ssa.gov

Social Security Administration. (2024). Actuarial life table. https://www.ssa.gov