Understanding When Roth Conversions in Retirement May Help Reduce Lifetime Taxes

One of the most common tax strategies retirees explore is Roth conversions in retirement.

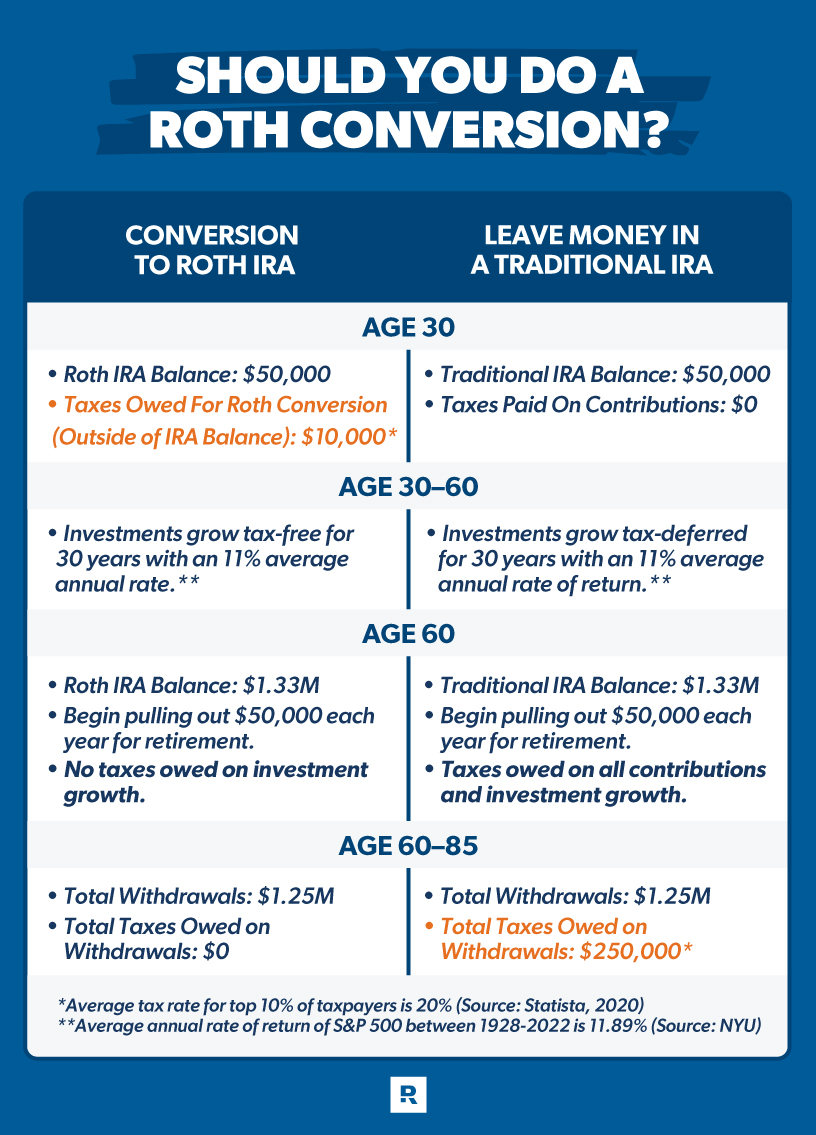

A Roth conversion involves moving money from a traditional retirement accounts, such as IRA or 401(k), into a Roth IRA. The amount converted is taxable in the year of the conversion, but future qualified withdrawals may be tax-free.

When used strategically, Roth conversions in retirement may:

-

Reduce future Required Minimum Distributions (RMDs)

-

Lower lifetime taxable income

-

Reduce the taxation of Social Security

-

Help manage Medicare premium thresholds

However, this strategy is not appropriate for everyone and should be evaluated carefully and discussed with your financial professional and CPA. Before implementing a conversion strategy, it’s important to avoid common tax planning mistakes retirees should avoid, especially when evaluating income thresholds and Medicare premium impacts.

How Roth Conversions in Retirement Work

When completing a Roth conversion:

-

Funds are transferred from a traditional IRA to a Roth IRA.

-

The converted amount is treated as ordinary income.

-

Taxes are due in the year of conversion. Taxes can be paid out of pocket or withheld from your conversion amount.

-

Future qualified withdrawals from the Roth IRA are generally tax-free.

(Source: Internal Revenue Service Publication 590-B, 2024)

When Roth Conversions in Retirement May Make Sense

1. During Lower Income Years

Early retirement before Social Security begins and before RMDs start may create an opportunity in a temporarily lower tax bracket. Converting during these years can help manage future RMDs. In some cases, (collaboration with your financial professional and CPA), you might be in a higher tax bracket, and it still might make sense to convert for another strategy specific to you and your life’s goals.

RMDs generally begin at age 73.

(Source: Internal Revenue Service RMD guidance, 2024)

2. To Reduce Future Required Minimum Distributions

Traditional IRAs require distributions starting at RMD age. Roth IRAs do not require RMDs during the original owner’s lifetime. Reducing pre-tax balances may lower forced future income. Many retirees evaluate Roth conversions as part of their broader retirement withdrawal strategies to create more tax flexibility over time.

3. To Manage Medicare Premiums (IRMAA)

Large RMDs later in retirement can increase Modified Adjusted Gross Income (MAGI), which may raise Medicare Part B and Part D premiums. Strategic Roth conversions in retirement may help smooth future income levels.

(Source: Centers for Medicare & Medicaid Services, 2024)

4. Estate Planning Considerations

Roth IRAs may provide tax advantages to heirs, as qualified distributions are generally income tax-free. However, beneficiaries are still subject to distribution rules under current law.

(Source: Internal Revenue Service, 2024)

When Roth Conversions in Retirement May Not Make Sense

Roth conversions in retirement may not be appropriate if:

-

You are already in a high tax bracket

-

You need the converted funds immediately

-

You do not have cash available to pay the taxes

-

The conversion would significantly increase Medicare premiums

Every conversion decision should be coordinated with a qualified tax professional.

Long-Term vs. Short-Term Thinking

A Roth conversion increases taxable income today.

The goal is not to avoid taxes; it is to manage them strategically over a lifetime.

Roth conversions in retirement are often about:

-

Filling up lower tax brackets intentionally

-

Creating tax diversification

-

Reducing uncertainty from future tax rate changes

Each retirement plan is unique. Incorporating conversions into your Annual Financial Review Checklist for Retirees ensures the strategy remains aligned with your tax bracket and long-term income goals.

Internal Revenue Service. (2024). Publication 590-B: Distributions from IRAs. https://www.irs.gov

Internal Revenue Service. (2024). Required minimum distributions. https://www.irs.gov

Centers for Medicare & Medicaid Services. (2024). Medicare premiums and IRMAA. https://www.medicare.gov