Why the Sequence of Returns Risk in Retirement Can Impact Your Income Plan

One of the most overlooked threats to retirement success is the Sequence of Returns Risk in Retirement.

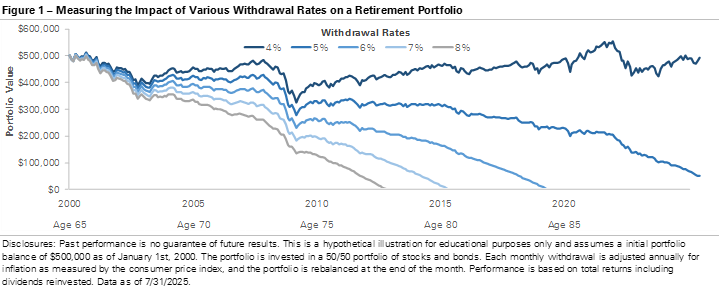

While many retirees focus on average market returns, the order in which those returns occur can significantly impact how long their portfolio lasts especially once withdrawals begin.

Understanding Sequence of Returns Risk in Retirement is essential when building a sustainable income strategy.

What Is Sequence of Returns Risk in Retirement?

Sequence of Returns Risk in Retirement refers to the danger that poor market performance early in retirement can permanently damage a portfolio when withdrawals are occurring.

Here’s why:

-

During working years, investors are contributing money.

-

In retirement, investors are withdrawing money.

-

If markets decline early while withdrawals continue, portfolio losses may compound.

Two retirees could earn the same average return over 20 years, but experience very different outcomes depending on the order of returns.

Why Sequence of Returns Risk in Retirement Matters

Once withdrawals begin, market losses have a larger impact because:

-

You’re selling investments while they are down. This makes it even more important to have a withdrawal strategy in place prior to retirement and taking distributions.

-

The portfolio has less time to recover

-

Withdrawals reduce the base that future growth compounds on

According to historical market data referenced by the U.S. Securities and Exchange Commission, market volatility is a normal part of investing.

The issue is not volatility itself; it’s volatility combined with withdrawals. This is why aligning withdrawals with your Safe Withdrawal Rate in Retirement is essential to portfolio sustainability.

A Simple Example

Imagine two retirees each starting with $1,000,000 and withdrawing $50,000 annually.

-

Retiree A experiences strong returns early, then weaker returns later.

-

Retiree B experiences weak returns early, then strong returns later.

Even if their average return is identical over time, Retiree B may deplete assets faster because losses occurred while withdrawals were happening.

This illustrates why Sequence of Returns Risk in Retirement is about timing and not averages.

Strategies to Help Manage Sequence of Returns Risk in Retirement

While no strategy eliminates risk, planning can help manage exposure.

1. Maintain a Cash or Short-Term Reserve

Holding one to three years of income needs in lower-volatility assets may reduce the need to sell equities during downturns. Inflation compounds this effect, making Inflation and Retirement planning equally important.

2. Flexible Withdrawal Strategy

Reducing withdrawals during market downturns may help preserve portfolio longevity.

3. Diversified Asset Allocation

Diversification across asset classes may reduce volatility over time.

The U.S. Securities and Exchange Commission emphasizes diversification as a foundational risk management principle.

4. Consider Guaranteed Income Sources

Social Security provides inflation-adjusted lifetime income. Delaying benefits increases monthly payments through delayed retirement credits.

(Source: Social Security Administration, 2024)

Having stable income sources can reduce pressure on investment portfolios during downturns.

Why Average Returns Can Be Misleading

Many retirement projections focus on long-term averages.

However, Sequence of Returns Risk in Retirement reminds us that the order of returns can matter more than the average — especially in the first 5–10 years of retirement.

Early planning and stress testing different market scenarios may improve confidence and income sustainability. Many early retirement missteps fall under broader Retirement Regrets and How to Avoid Them discussions.

Every retirement income plan should be reviewed alongside your financial professional to ensure it aligns with your goals and risk tolerance.

Sources

U.S. Securities and Exchange Commission. (2024). Saving and investing basics. https://www.sec.gov

Social Security Administration. (2024). Retirement benefits planner. https://www.ssa.gov